Small Claims Court As Last Resort – Know Your Consumer Rights! They say knowledge is power. It certainly is when it comes to your consumer rights. Knowing what you are legally entitled to and how to put your rights into action, can possibly save you from having to take your claim through the small claims court and save you money!

Over the years I have fought many consumer rights claims. These have included getting compensation as my electric wheelchair caused £4000 damage to my home and getting a full refund from a holiday park disaster! I’ve learned so much and a few tips along the way. Sharing what I have done, I hope helps you too. I will say though, it’s not an easy task and you do need to have the patience of a saint and more importantly, the determination to see it through to the end.

What Is The Consumer Rights Act?

The Consumer Rights Act came into force on 1 October 2015. This meant from that date new consumer rights became law covering:

- what should happen when goods are faulty;

- what should happen when digital content is faulty;

- how services should match up to what has been agreed, and what should happen when they do not, or when they are not provided with reasonable care and skill;

- unfair terms in a contract;

- what happens when a business is acting in a way which isn’t competitive;

- written notice for routine inspections by public enforcers, such as Trading Standards; and

- greater flexibility for public enforcers, such as Trading Standards, to respond to breaches of consumer law, such as seeking redress for consumers who have suffered harm.

Most of these changes were important updates to existing laws. But two new areas of law were also introduced.

- For the first time rights on digital content have been set out in legislation. The Act gives consumers a clear right to the repair or replacement of faulty digital content, such as online films and games, music downloads and e-books. The law here had been unclear and this change has brought us up to date with how digital products have evolved.

- There are now also new, clear rules for what should happen if a service is not provided with reasonable care and skill or as agreed. For example, the business that provided the service must bring it into line with what was agreed with the customer or, if this is not practical, must give some money back.

The Consumer Rights Act 2015 stands alongside Regulations to create a greatly simplified body of consumer law. Taken together, they set out the basic rules which govern how consumers buy and businesses sell to them in the UK.

Source: CAB

How Can I Limit Things Going Wrong?

There are several things you can do to help limit the chances of things going wrong:

- Purchase items from trusted sources, especially if buying online

- Use Paypal where you can for your purchases – Paypal offer buyer protection (exclusions apply)

- When spending £100 or more & up to £30,000, use a credit card. Your credit card company has a LEGAL responsibility to come to the rescue if there’s a problem, called (section 75)

- Debit cards offer less protection but do have a chargeback facility for purchases under £100

- Look out for scams. These can be via text and/or emails

- Read a companies T&Cs, delivery & returns policies

- Record your phone calls – No, it’s not illegal in the UK

- Always try resolving your issue with the company/seller first

Trusted Sellers

We have all at one point or another bought products online. How can you tell if a company/seller is legit? It can be a minefield and sometimes challenging to tell.

- Using the company name – Visiting Trustpilot is an excellent way to see if others have bought from them and what they say. Stupidly I only visited Trustpilot once things went wrong with one purchase, to find the reviews had been awful. I didn’t make that mistake again! Also, I stay away from companies/sellers that have 0 reviews.

- Facebook is famous for pop-up sellers (not Marketplace). I’m talking about the ads in your timeline advertising wonderful inventions that make you look younger, thinner, richer etc. – I bought make-up from one of these sellers and had to go through Paypal to get my money back as I never received my items. When searching for the company website, (where bought the products from) it had disappeared overnight! Another tip, look on Amazon or eBay, I bet you’ll find the same product there too and be better protected.

- Places like eBay, Amazon and high street shops are always the best way to make purchases. They come with their own T&C and you are protected if/when things do go wrong. I have found Amazon to be the easiest place if needing to return anything.

Paypal

Buyer Protection covers all eligible purchases where PayPal is used, as well as payments made through our website. To take advantage of Buyer Protection, we require, among other things, that PayPal accounts be kept in good standing and ask that a dispute be filed within 180 days of your purchase or payment, Terms and Conditions apply.

I have used Paypal in the past when things have gone wrong with sellers. You have to obviously fill in a form with all the information. Put in everything, even if you don’t think it’s relevant. You want to make sure you give Paypal everything they need. You literally get one shot at putting your case across! I have had them refuse my claim as I didn’t include enough info.

Source: Paypal

What Is A Chargeback?

Chargeback allows you to ask your card provider to give you a refund on your credit or debit card if the goods or services you bought don’t arrive, are faulty or don’t match the description of what you ordered.

When a card transaction is disputed, you may be able to use chargeback to reverse the payment and recoup your money.

How Does It Work?

A chargeback happens when the bank removes the funds from the retailer’s bank account and returns them to you – although this can be challenged by the retailer if they feel the claim is unjustified.

Chargeback is a voluntary scheme. It is not the same as claiming money back under Section 75 (more on that in a moment).

Am I Eligible To Make A Claim?

If goods or services you bought with a card either don’t turn up, are faulty or damaged, or if they are different from the description then you may have a case to make a chargeback claim.

You should first try to get a refund from the retailer. If they refuse or if they have gone bust, you can contact your debit or credit card provider, who will then contact the retailer’s bank to make the claim.

Chargeback could also be used should the retailer charge you multiple times for the same item, if they go into administration or even if you have been the victim of fraud and did not authorise the payment.

Source: Moneysupermarket

What Is A Section 75

Section 75 is an important UK consumer protection law made in the 1970s that means your credit provider must take the same responsibility as the retailer if things go wrong with a purchase. Yet it doesn’t work on all purchases – just those costing a certain amount:

Buy something costing more than £100 and less than £30,000 on your credit card, and your card company has a LEGAL responsibility to come to the rescue if there’s a problem.

- If there’s a problem with something you’ve bought on credit. The lender is as responsible for putting things right as the company you bought from. In other words, if what you’ve bought is faulty, broken or doesn’t arrive. The credit provider is legally obliged to put it right (see our Consumer Rights guide for exact definitions).

- For Section 75 to work, there has to be a direct link between you, the creditor (usually your credit card issuer), and the supplier (the place you’re buying from). For example, something you bought in a shop with a credit card would be covered, but if you used your credit card to withdraw cash from an ATM and then spent it on the same item, you wouldn’t be protected by Section 75 as the direct link would have been broken. See a detailed breakdown of what Section 75 covers.

- The product or service you’re buying must cost over £100 and not more than £30,000 to be covered. Crucially, though, you’re still covered even if you only pay a deposit of 1p towards an eligible purchase on credit. You’re also covered if you’ve since closed the credit account you made the purchase with.

Find out how to make a Section 75 claim.

Source: Moneysavingexpert

Recording Phone Calls

We have all thought about it at some point, whether it’s for proof of what was said during an argument or to just record a meeting or conversation, but is recording conversations actually legal?

When it comes to discreetly recording conversations, calls or even filming someone, the law in the UK varies between individuals and businesses and it’s important to understand the distinctions before you attempt it.

Nowadays, the range of technology at our disposal means it is easy to record conversations without the other participant’s knowledge – but does that mean it’s ethical, and can it be admitted as evidence in court? (Most mobiles today have a built-in phone recorder, you just need to switch it on).

(I have recently taken to recording all my calls made to companies. My claim against Palins holiday park would have been much easier had I recorded my initial phone call with them. I was told some information on the phone that was not true. When I made my initial complaint, it was denied that I had even been told this).

Is It Illegal To Record A Conversation In Secret?

Recording a conversation in secret is not a criminal offence and is not prohibited. As long as the recording is for personal use you don’t need to obtain consent or let the other person know.

Things change if the matter is addressed with a claim for damages or if the recordings have been shared without the consent of the participants. Even worse, if the recording is sold to third parties or released in public without the consent of the participants then this could be considered a criminal offence.

Can A Private Recording Be Submitted As Evidence In Court?

A private recording can be submitted as evidence, but with some conditions:

- A recording may be relied on in evidence if the court gives permission

- An application for permission should be made on form C2

- The recording should be made available to other parties before any hearing to consider its admissibility.

Covert recordings of children should rarely if ever, be admitted as evidence, according to section 13(4) of the Children and Families Act 2014.

Source: DMA Law (UK)

Scams

How on earth can you tell if something is a scam?

- Cold calls or unexpected emails or messages should raise suspicion, especially if you’re asked to give personal or payment details. It’s very unusual for legitimate organisations to contact you and ask for sensitive information if you’re not expecting them to. If you’re not 100% convinced about the identity of the caller, hang up and contact the company directly.

- Never share your personal details with anyone if you can’t confirm they are who they say they are. Phone scammers will often try and get valuable personal data from you.

- Scam websites often have vague contact details. PO box, premium rate number (starting ‘09’) or a mobile number. If anything goes wrong it’s important you can contact those involved. This will be difficult if you don’t have accurate contact information.

- It’s important you can discuss any agreements with your friends, family or advisors. Asking you to keep quiet is a way to keep you away from the advice and support you need in making a decision.

- Scams will often promise high returns for very little financial commitment. They may even say that a deal is too good to miss. Use your common sense, if a deal is too good to be true, it inevitably is.

- Fraudsters often try to hurry your decision-making. Don’t let anyone make you feel under pressure – it’s OK to take a break and think things through if you’re not sure.

- Emails or messages littered with spelling and grammar mistakes are scam giveaways. Legitimate organisations will rarely if ever, make spelling or grammatical mistakes in their emails to you because they’ve been put together by professionals and checked before they’re sent.

What to do if you’ve been scammed

Fraudsters are very cunning in their tactics so it’s not always immediately obvious that you’ve been scammed, or who you should report it to.

But there are ways to identify different types of scams, and organisations that can help you if you are scammed. Read the following guides to find out more…

Source: Which

Wording & Facts

In my experience, how you put yourself across (knowing your rights and being factual), is probably the most important but hardest part of all, in fighting for your consumer rights.

I remember a case my husband was trying to win regarding a caravan fire. He wasn’t able to convey the case very well but as it was his Dad’s caravan, I didn’t want to butt in too much. The insurance company took this opportunity to fob him off with a pittance amount of compensation. (This actually went against what was written in the policy his Dad took out with the company).

In the end, I took over as I felt hubby had struggled enough in these phone calls and was annoyed by how the insurance company was abusing his lack of knowledge against him.

The gentleman I spoke to unbelievably, turned round to me and said, “oh, I can see I’m talking to someone who knows what they’re doing”. (The cheek). I have to say I was quite taken aback by this comment but needless to say, happy as the company was now aware they weren’t going to be able to fob us off anymore! The result was the company offering nine times the amount they had previously offered. 1 up to the consumer!

A recent claim of ours, a Section 75 claim regarding our holiday park nightmare. The correct words were not used in describing why we wanted a section 75 claim, this resulted in the credit card company saying we didn’t have a claim to take forward. After doing more research, we found the correct terminology and contacted the CC company again, who this time took the case and we won.

Research & Determination

I can’t stress enough about researching whatever your particular consumer issue is. It will be the basis of your claim/case.

- Read other consumer stories similar to yours

- Look up legal websites that may offer some free tips etc.

- Write/type down your thoughts, snippets of information you may find, legal terminology you want to use

- Make sure you use consumer rights jargon (no, it’s not as complicated as it sounds, copy/paste is a wonderful feature). Not fit for purpose, not as described and breach of contract are some of the consumer rights jargon that will get most companies etc. attention. (Making sure you use the right one is the key).

- Make drafts of letters/email before sending. For any and all correspondence you send or receive, make sure to keep copies. Keep them somewhere safe. You may need them as proof or to refer back to at a later date.

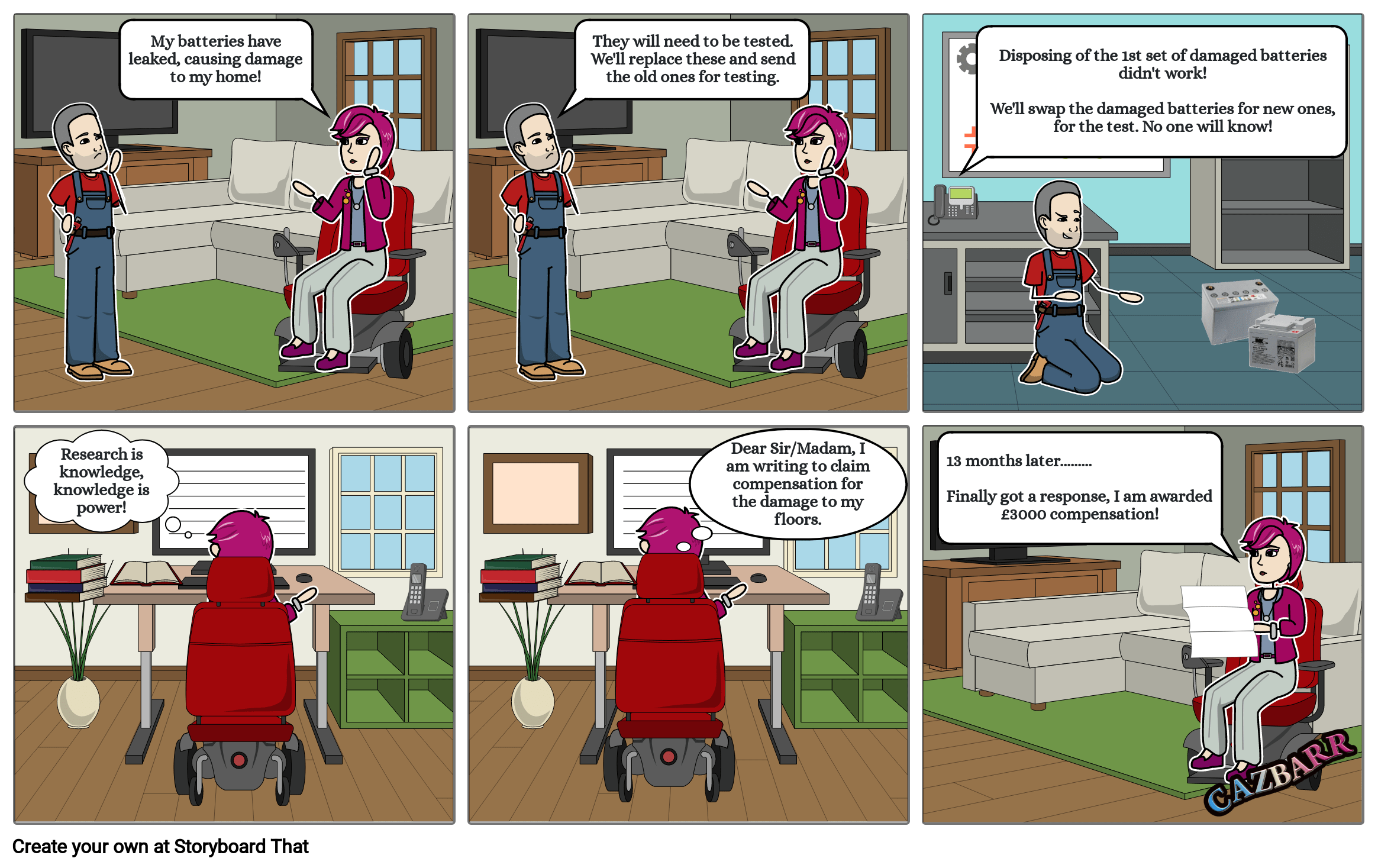

If you are trying to win a claim of a significant amount, be prepared for it to take some time. My claim for £4000 from my wheelchair repairers took 13 months. If you read my NHS wheelchair service: Is yours “fit for purpose”? blog, you will see why it took so long and the type of consumer rights terminology I used. Some companies will most definitely drag their feet in the hope you will give up…..DON’T!!!

* Disclaimer

All information supplied, is for consumers based in the UK. While every effort‘s been made to ensure the information in my blog is accurate. It doesn’t constitute legal advice tailored to your individual circumstances. If you act on it, you acknowledge that you do so at your own risk. I can’t assume responsibility and don’t accept liability for any damage or loss which may arise as a result of your reliance upon it. Please speak with a solicitor specialising in consumer law to get professional advice.

About Cazbarr

Cazbarr is a full-time wheelchair user, who was born with a disability called Arthrogryposis. Primarily she blogs about her disability, her experiences holidaying as a full-time wheelchair user, along with honest products & service reviews.

If you would like to work with Cazbarr, just drop her line on the Contact page.